The Summer of Our Discontent?

Navigating Maximum Market Uncertainty as Private Company Valuations Hang in the Balance

By: Gary Moon, Managing Partner, Nfluence Partners

gary@nfluencepartners.com

As stocks tumble and interest rates rise, private company executives and investors are scratching their heads on capital availability and valuations. Whether or when we are heading into a recession has become the question of the year, and many feel as though there is no solid ground in either the public or private markets. While it is wise to be cautious and examine assumptions, we believe this volatile period represents more of a valuation recalibration and capital deployment momentum shift than an overall dealmaking collapse as investors triage portfolio companies and prepare for the potential of increased difficulty to come. Volatility can be scary, but it does not last forever.

Maneuvering Through the Current State of the Market

While the public market has endured falling stocks and billions in losses this year, the private capital market continues to experience VC-backed company layoffs and delayed fundraises.[1] The knock-on effects from falling valuations in the public market can already be seen permeating the private market. Many B2C companies, already challenged by seismic changes to the customer acquisition landscape, are falling further behind as consumers tighten their belts to combat layoffs, inflation, and tumbling 401Ks. In direct correlation, B2B2C companies are already facing — or are bracing themselves for — the trickle-down effects of decreased consumer spending power. On the bright side, B2B companies (outside of marketing and advertising sensitive businesses) have largely been insulated from the turbulence thus far — a sign that this is not an unsalvageable economic catastrophe in the broadest sense (yet).

On the private capital provider side, firms up and down the spectrum have been looking inward. With the market in bear territory, GPs are conducting a comprehensive analysis of their portfolio companies to decipher precisely where they should allocate resources and just how much cash burn can be cut before they need to take more drastic measures. The riotous multitudes of companies with astronomical burn rates are facing a landing zone of lower valuations back here on Earth. Capital allocation has shifted away from the “growth at any cost” mentality as companies look to spend money more wisely. Deal flow has slowed, partly because firms are focused on portfolio stabilization and partly because they are struggling to price new deals in this oversold market.

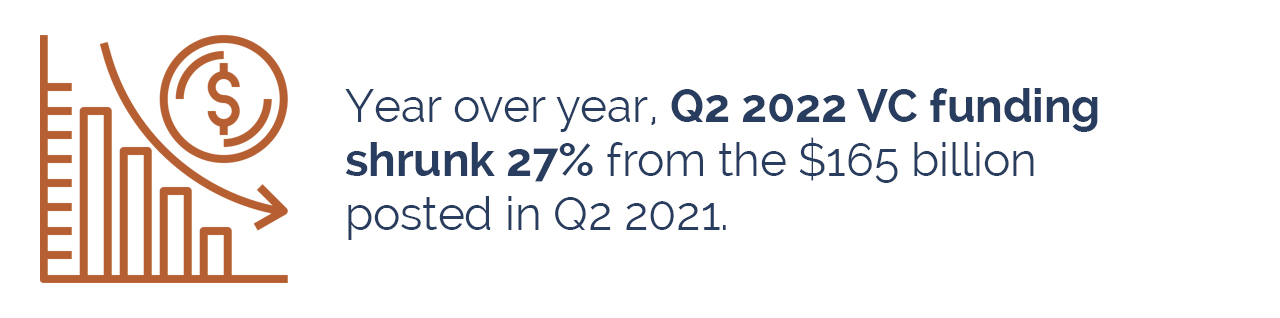

Venture capital funding has been steadily declining through the first half of 2022. In May, global venture funding for the month dipped to $39 billion, its first monthly weigh-in under $40 billion in over a year.[2] Second-quarter funding dropped 26% from $162 billion in the first quarter. Year over year, Q2 2022 VC funding shrunk 27% from the $165 billion posted in Q2 2021.[3]

Although the potential for growth could be on the horizon for private equity firms with record-high levels of dry powder ($975 billion, to be exact[4]), it seems that dealmaking and portco firefighting are not like walking and chewing gum at the same time. The velocity of the dry powder getting called up to bat is slowing — a large fund in 2021 would’ve reached deployment between 12 to 18 months, but as we speed through Q3 of 2022, these funds may revert to the more traditional three years before they are fully deployed, depending on how the macro-economic picture plays out.

Fundraising itself may also become a near-term issue for private capital firms. As allocations to public markets decrease in value, LPs will begin to face an unbalanced scale of private market allocations and therefore have less wiggle room to invest. In fact, almost a fifth of institutional investors plan to decrease their commitments to private equity over the next 12 months, according to research from one fundraising advisory firm.[5] On the VC side of the market, fears of recession and dealmaking troubles have triggered an increase in pessimism on private market portfolios. Data from Q1 shows markdowns in net asset values have already started, with 68.1% of VC funds showing a drop in valuations from 2021.[6]

Much of the venture growth market has slowed or halted altogether due to cooling investor confidence and portfolio triage amid market volatility. While the top 20% of companies are still closing new financing rounds, the “venture capital on the beach this summer” memes ring true. With much of the energy being consumed in portfolio review and recalibration, we expect this market to be the last to settle into a new normal, and it may take much of the fall to shake itself out. Yet shake out it will, with record amounts of VC dry powder still waiting to be deployed.

Private equity platform deals continue to see high levels of activity and interest. With record capital availability, less sensitivity to valuation fluctuations, and lower overall utilization of debt, we see only minor impacts when compared to a fully functioning market.

Lastly, strategic acquisition activity is ruled by specificity — each deal depends on factors such as the specific company or sector dynamics, runway, and hold-period timing considerations. Public acquirers with significant cash remain active and in fact may increase activity given a more favorable valuation environment. Those without significant cash are on the sidelines, reticent to use deeply discounted stock as consideration. Private equity-backed platforms, much like the PE market, continue to be strong.

At the same time, “What anything is worth?” is the question of the summer, with firms taking dramatically different approaches — from opportunism to realism and reversion to a mean in a hyper-competitive market — to invest in the highest quality firms.

Business owners thinking about selling may also face a complex set of decisions. Although investors may have valued their business at a desirable multiple 12 months ago, they may now need to sell at a lower mark in order to get a deal done before potential further degradation of value or wait until the market rebounds. Again, these decisions are highly impacted by the business’s vertical and sub-vertical consolidation trends.

So, Is There Any Good News?

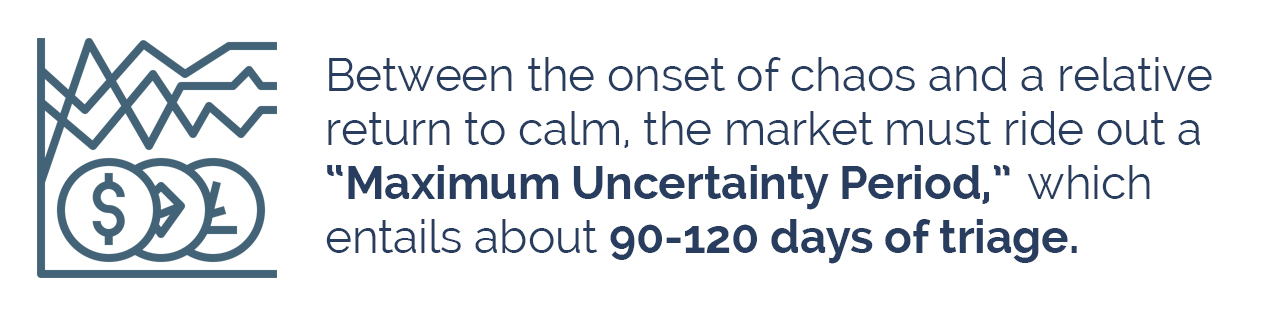

Even though the market forecast may seem questionable, there is good news: We’ve experienced this before. The economic cycles that fluctuate between high growth and recession are actually healthy and to be expected. Between the onset of chaos and a relative return to calm, the market must ride out a “Maximum Uncertainty Period,” which entails about 90-120 days of triage. This market correction is certainly not our first — in fact, much of our senior team has guided our companies and our clients through three separate eras of market instability and massive correction before this one, starting with the Dotcom Bubble in 2000. As everyone pontificates on patterns within prior cycles, none serve precisely, and each has interesting parallels from which to learn.

2020: Capital Availability and Sector-Specificity

When COVID sent the stock markets tumbling in 2020, a relevant pattern for this summer of uncertainty was established — valuations dropped, dealmaking hit pause, and portfolio companies found themselves under the GP’s microscope. As the Federal Reserve System kept interest rates at historical lows and started pumping capital into the economy, investors quickly moved attention and capital into those companies most accelerated by the Pandemic. Tech was already eating the world, and these dynamics accelerated its consumption.

Nevertheless, by August and September of 2020, the market had recalibrated and reset. The triaging of portfolio companies, although seemingly a red flag for the market, came and went in a fleeting few months. In late 2021, a New York Times article noted that “each bout of pandemic-driven volatility in the stock market since February 2020 has been shorter than the one before and followed by a recovery to a new high.”[7] Although the market may be unsteady now, there is a precedent that “The Maximum Uncertainty Period” can fizzle out in short order and that the market is likely to recalibrate by the fall.

2007-2009: Systemic Collapse

The Great Recession represented a broader-based economic impact – driven by larger, systemic challenges in the financial ecosystem with global ripple effects. The private capital markets are markedly more robust today than they were then. In early 2009, PE fund dry powder hovered around $1 trillion[8] as compared to $3.6 trillion today.[9] Venture capital firms globally raised $49.4 billion in aggregate in 2008, while VC funds raised over $70 billion in commitments in the first quarter of this year alone.[10]

2000-2002: Double Impact

While many have looked even further back to the Tech Bubble in 2000 – 2002, remember that while tech companies were hopes and dreams back then, today, they are significant and real. Additionally, the VC and PE markets were an order of magnitude smaller (VC funds only raised $1.4 billion in 2001[11]), and the Dotcom Bubble bursting was promptly followed by the second and more significant economic shock of 9/11, extending and deepening its impacts.

For now, those who are more disciplined in managing cash burn and sticking to valuations that likely revert to a mean will find more stability and a continuation of strong deal flow moving into 2023.

Our recommendation? Take a deep breath, hold on, and believe that “this too shall pass.” Our team is here to help you think through the nuanced impacts on your company or portfolio — reach out any time.

[1] PitchBook Analyst Note: Analysts Advise on Key Trends to Watch as Markets Return to Turmoil

[2] The VC Reset: May 2022 Funding Falls Again, But Not At Every Stage

[3] Q2 VC Funding Globally Falls Significantly As Startup Investors Pull Back

[4] Private equity: Deals 2022 Midyear Outlook

[5] Private equity liquidity sees record fall as LP sentiment heralds tougher fundraising

[6] PitchBook Analyst Note: Did VC Fly Too Close to the Sun?

[7] The Stock Market’s Covid Pattern: Faster Recovery From Each Panic

[8] Dry Powder Available to PE Fund Managers Tops $1 Trillion as 2008 PE Global Fundraising Hits $554bn

[9] Shifting Gears: Private Equity Report Midyear 2022

[10] High hopes and a mountain of dry powder have VCs poised for a soft landing

[11] VC funds raised $1.4 billion in 2001, 63% less than 2000